Wealthy clients today face serious issues. At the top of the list is how to keep their families wealthy for generations to come while enduring the simultaneous problems of low interest rates on deposits and the generational erosion of assets due to the federal estate tax. Ouch.

By way of background, the federal estate tax was changed significantly in 2009.

Today’s wealthy clients understand that they have a $5 million exemption per person. For married couples, that’s $10 million that can be passed on to the next generation net of tax with proper planning.

At least for now.

But in a revenue-hungry, government-centric environment where Congress is searching for every tax dollar, how long will such an exemption last? One year? The next election cycle? Ten years? No one knows for sure. What we do know for sure is that the federal estate tax has been changed time and time again.

In regard to interest rates, the prevailing wisdom is that they will increase in the future from today’s minuscule savings rates. According to Bankrate.com as of this writing, the average money market bank fund in America pays a paltry 0.48 percent. A one-year certificate of deposit pays 0.71 percent, and a five-year CD pays a whopping 1.5 percent. None of these rates comes close to keeping up with inflation as measured by the U.S. Consumer Price Index.

Many wealthy clients who have significant liquid assets are considering using a high early value life insurance policy as an alternative to such low savings rates – especially if they have a potential future drain on their assets caused by estate taxes.

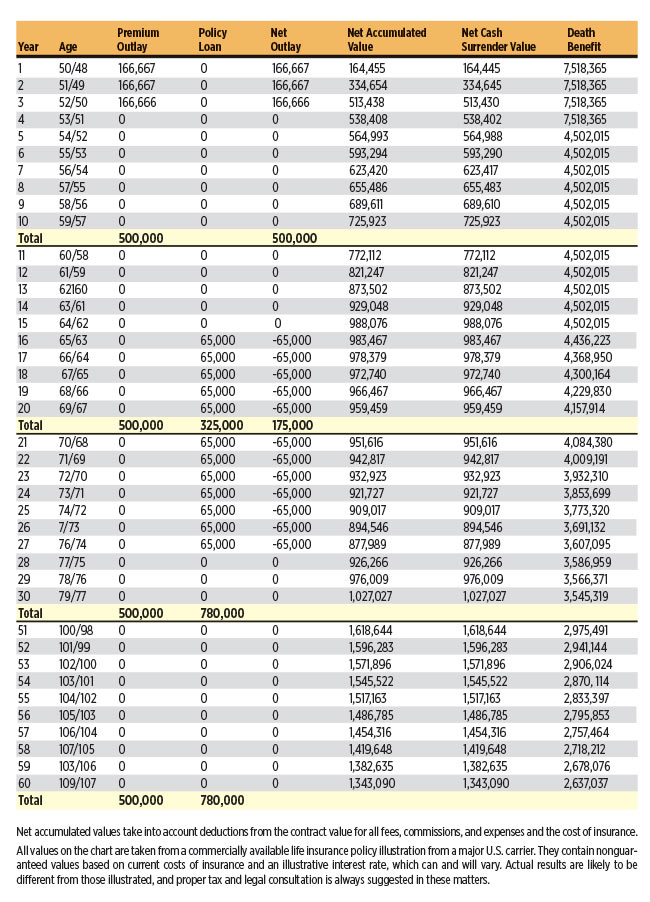

The chart on the next page (pg. 42) shows the impact for Bob, 50, and his wife, Betty, 48, when they reposition $500,000 from their bank money market account (in equal installments of about $166,667) over a scant three years into such a plan.

If a bank would pay a 1 percent interest rate on a savings account, the interest “loss” to Bob and Betty on that $500,000 after the deposits is $5,000 yearly. Or is it? In a commercially available second-to-die indexed universal life insurance policy from a strongly rated carrier, the fifth-year cash value based on a midpoint interest rate of 6.5 percent (below the actual history of the carrier as of 2013) is $564,988, more than the same stream of payments compounded at 1 percent interest over the same time frame. By the way, if Bob and Betty are high-tax-bracket folks, and they probably are, their bank interest is taxable – making the difference in favor of the life insurance policy even more substantial.

Perhaps more important, the second-to-die estate (death) benefit in that policy is some $4,502,015 in Year 5. That’s nine times their deposits.

If the policy is personally owned, Bob and Betty have access to their cash value at any time, via withdrawal or through a low-interest policy loan. At any point, the policy could be used as collateral for a business loan should Bob and Betty decide on a potential venture. All cash values accumulate free of tax until withdrawal, and withdrawals may be tax-free, if properly structured, under current tax rules.

Here may be the best part. When Bob reaches age 65, the life insurance policy can begin distributions on a tax-free basis under current law. In this example, a $65,000 annual withdrawal occurs each year over the next 12 years (assuming that midpoint interest rate and current insurance/administrative charges). That’s $780,000 of tax-free withdrawals from their initial $500,000 deposit – some $280,000 more than they put in, potentially income tax-free.

Now, when they reach ages 77 and 75, respectively, Bob and Betty can maintain the life insurance policy with its death benefit in excess of $3 million without any further deposits under those same assumptions for the remainder of their lives.

If Bob and Betty should change their minds a few years down the road, it seems unlikely they would lose any return whatsoever in comparison to a bank account. Looking at the market history of the various indexes even in recent tumultuous years, Bob and Betty would likely still be ahead of where they would’ve been at today’s paltry money market rates, especially because they can never earn a negative return in today’s policies of this type.

If the estate tax laws are changed to reduce the $5 million exemption to, say, $1 million or some other number, this policy could be placed into an irrevocable trust using part of Bob and Betty’s lifetime unified credit at some point in the future.

Or Bob and Betty could choose to donate the policy to a charity. They would receive a significant income tax deduction while the charity receives a significant windfall.

And in some states, life insurance has significant insulation from creditors.

Leveraging low-interest and, in many cases, dormant bank savings into large life insurance policies with high early values could be the right solution for today’s wealthy client.

Source:(http://insurancenewsnetmagazine.com/article/leveraging-low-interest-rates-to-avoid-an-escalating-estate-tax-2833)

Be the first to comment on "Leveraging Low Interest Rates to Avoid an Escalating Estate Tax"